Written Commentary

Soybeans and soymeal traded sharply lower. Corn and soyoil also traded lower. Chicago wheat managed small gains. US stocks were higher. Crude was lower. Dollar was mixed.

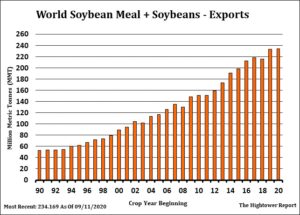

SOYBEANS

Soybeans trade sharply lower. Fact USDA was closed for holiday limited new news for the bulls. SX lower trade erased all of USDA Fridays gains. Some feel uncertainty over South America weather and record US Oct-Jan soybean exports could keep SX in a 10.10-10.80 range. US 2020/21 soybean supply and demand has tightened to the point South America and US will need good crop to satisfy demand. In April, SX was near 8.31 low. Dry US Aug weather and China buying helped SX rally to recent thigh near 10.79. On Friday, USDA estimated World 2020/21 soybean exports near 167.9 mmt versus 166.3 estimated in Sep and 164.5 last year. US is 59.8 versus 57.8 previous and 45.6 last year. Some feel US exports could even reach 64.0. Brazil exports are estimated near 85.0 versus 92.5 last year. China soybean imports are estimated near 100 mmt versus 97.4 last year. Argentina soymeal exports are estimated near 29.0 mmt versus 26.7 last year. US soymeal exports are estimated near 12.2 mmt versus 12.6 last year.

CORN

Corn traded lower. Fact USDA was closed today due to holiday limited new news for the bulls. Most look for US corn harvest to be near 45-50 pct done. CZ had an inside day and erased all of Fridays USDA report gains. Tighter US 2020/21 supply and demand outlook and uncertain Argentina weather could still offer support. Lack of US and Argentina farmer selling also could be supportive. Some feel CZ will now settle in a 3.70-4.05 range. In April, June and August CZ dropped to a low near 3.20. Dry US August helped CZ rally to recent high near 3.98. FSA enrolled aces was near 88.1 million acres versus 87.6 last month. This is 96.9 pct of USDA planted acres guess and suggest there acres could be right. 6.17 million corn acres is in prevent plant. On Friday, USDA estimated World 2020/21 corn exports near 184.4 mmt versus 186.0 estimated in Sep and 170.5 last year. US is 59.0 versus 45.1 last year. Some feel US exports could even reach 64.7. Brazil exports are estimated near 39.0 versus 34.0 last year. Ukraine exports are estimated near 30.5 mmt versus 32.5 previous and 29.2 last year. Argentina exports are estimated near 34.0 mmt versus 38.0 last year.

WHEAT

Wheat futures traded mixed. WZ is near 5.96. WN21 is near 5.95. KWZ is near 5.30. KWN is near 5.51. Interesting to note that historically, nearby Chicago wheat has a key price near 6.00. Above that price and prices tend to rally. Mostly due to drop in global supply. Trade below 6.00 and prices tends to trade lower. This usually due to increase global supply. USDA estimates World 2020/21 crop near 773.0 mmt versus 764.5 last year. It remain dry in Russia, Argentina and US south plains. Russia could see some showers but most do not feel there is a pattern change. Potential drop in US Dollar could support prices. Talk of a vaccine and inflation could also help prices. Some look for US 2021 wheat acres to be near 45.4 million versus 44.3 this year. This could produce a crop near 1,960 mil bu versus 1,826 this past year and a carryout near 934 versus 883 last year. On Friday, USDA estimated World 2020/21 wheat exports near 189.9 mmt versus 189.4 estimated in Sep and 190.5 last year. Russia is 39.0 versus 34.4 last year, EU is 25.5 versus 38.4, Canada is 25.0 versus 24.6, US is 26.5 versus 26.3 last year, Australia is 19.0 versus 9.5 and Argentina is 13.0 versus 13.5.